|

|

新國CPF最新宣傳短片,色鹿會看了老淚縱橫嗎?

[复制链接]

|

|

|

发表于 23-3-2017 12:12 AM

来自手机

|

显示全部楼层

发表于 23-3-2017 12:12 AM

来自手机

|

显示全部楼层

afei25 发表于 22-3-2017 11:51 PM

放心吧,游戏规则他们已经定好啦,提高保险费就是一招。到你65岁时,一年医保费10千,不到5年你的medisave 全部被他们吃掉咯。不需要你拿出来。

唉 只能望着自己的 cpf statement...

看内面有偌济钱... |

|

|

|

|

|

|

|

|

|

|

|

发表于 23-3-2017 04:33 AM

来自手机

|

显示全部楼层

afei25 发表于 22-3-2017 11:51 PM

放心吧,游戏规则他们已经定好啦,提高保险费就是一招。到你65岁时,一年医保费10千,不到5年你的medisave 全部被他们吃掉咯。不需要你拿出来。

乱说话。

|

|

|

|

|

|

|

|

|

|

|

|

发表于 23-3-2017 08:13 AM

|

显示全部楼层

看你站在那个角度看吧。

假如我今天55岁:

加上 basic healtcare sum 的5万2千 (这个只有到65岁才不会增加)

假如我选brs, 83000+52000, 这笔不能提出来的钱,都是近10年来我cpf的利息和雇主给于的,我连1分钱都不用留在cpf内。

|

|

|

|

|

|

|

|

|

|

|

|

发表于 23-3-2017 09:21 AM

|

显示全部楼层

射了,所以特别清醒.

|

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 23-3-2017 04:15 PM

|

显示全部楼层

色鹿對債券不熟悉!

買賣政府債券(SGS BONDS)不需要付費,也沒有手續費和管理費!

買賣SGX上市債券(SGX LISTED BONDS)需要付費,但放在CDP沒有管理費!

|

|

|

|

|

|

|

|

|

|

|

|

发表于 23-3-2017 05:41 PM

|

显示全部楼层

我不熟悉政府债卷,但几个月前曾经看过singapore saving bonds,利息不吸引人,也需要手续费。

|

|

|

|

|

|

|

|

|

|

|

|

发表于 23-3-2017 05:58 PM

来自手机

|

显示全部楼层

本帖最后由 山地居民 于 23-3-2017 06:00 PM 编辑

kcchiew 发表于 23-3-2017 05:41 PM

我不熟悉政府债卷,但几个月前曾经看过singapore saving bonds,利息不吸引人,也需要手续费。

還好,去年的普遍很低 |

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 24-3-2017 02:11 PM

|

显示全部楼层

SSB 買賣只收2元!

SSB當然不能和CPF比!

但SSB可以完全拿出來!CPF不能!

|

|

|

|

|

|

|

|

|

|

|

|

发表于 24-3-2017 11:49 PM

|

显示全部楼层

SINGTEL 10年 债券 3.25%, 但不清楚需要什么费用。UOB 的 有4%, 好像都高过CPF 的 2.5%

|

|

|

|

|

|

|

|

|

|

|

|

发表于 25-3-2017 01:34 AM

来自手机

|

显示全部楼层

本帖最后由 kcchiew 于 25-3-2017 01:37 AM 编辑

gonong 发表于 24-3-2017 02:11 PM

SSB 買賣只收2元!

SSB當然不能和CPF比!

但SSB可以完全拿出來!CPF不能!

如果我今年55岁, 我不介意把24万9千新元投入年金计划, 因为65~70岁后我将提更多的年金, 直到我离开人世为止。

这才叫老年规划。

而且, 你只要在市场上可以找到比cpf life回报更好的年金计划, 你能选择不跟cpf买。 |

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 27-3-2017 01:51 PM

|

显示全部楼层

這些都是250K一粒的“公司債券”!

只需要付買或賣的手續費,沒有其他費用!

通常優質的比如銀行有4到5%回報!

超過5%要小心!

|

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 27-3-2017 01:52 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 27-3-2017 02:34 PM

|

显示全部楼层

不是很清楚,这新的选择是2016年1月刚开始的。

去年的年报有这么说:

。。。By end March 2016, we

saw over 4,000 top-ups by members above the age of 55 to

the current Enhanced Retirement Sum (ERS), with a total top-up

sum of $185.5 million. 。。。

那些可能是快要拿钱的(65岁)会员。

人都是这样的,还没到时就以为自己活不了多久,等到活到那个年份的时候,就感觉钱不够用了。

|

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 27-3-2017 03:53 PM

|

显示全部楼层

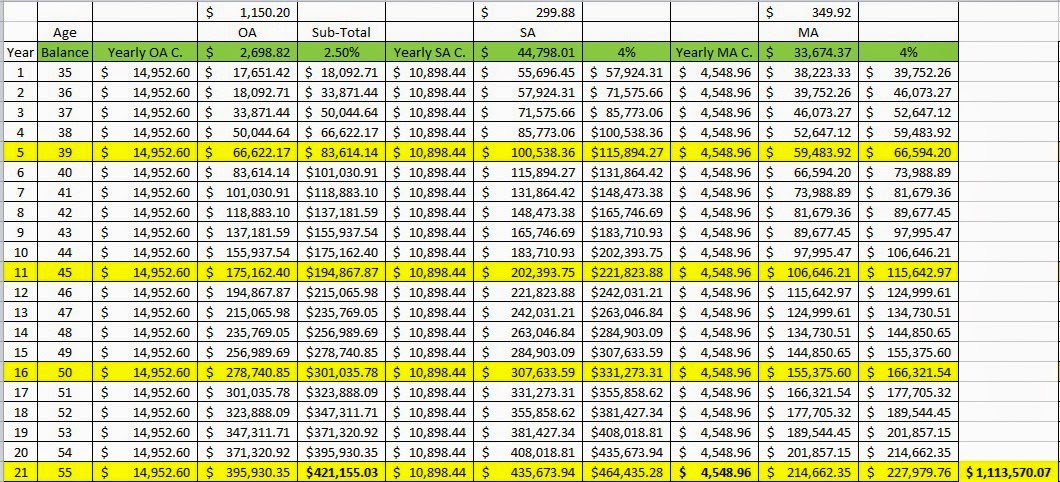

如果你55歲時候和下面圖表一樣多錢,那麼ERS就是你說的“免費”利息錢!

|

|

|

|

|

|

|

|

|

|

|

|

发表于 27-3-2017 05:02 PM

|

显示全部楼层

本帖最后由 kcchiew 于 27-3-2017 05:03 PM 编辑

sa和ma算法有错误。

ma到顶的话,利息会转到sa和oa。假如sa也到顶,ma的利息就只去oa。

sa到顶,就不能把oa的钱转入该户口,每个月工作的sa contribution 只有几百块罢了。

总而言之,只要sa和ma到顶,就没有办法把自己oa的钱转进sa和ma,利息“亏”很多,新加坡政府不让我们通过cpf“赚”更多钱。

|

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 29-3-2017 05:48 PM

|

显示全部楼层

對!只有SA或RA能拿到最低4%年率!

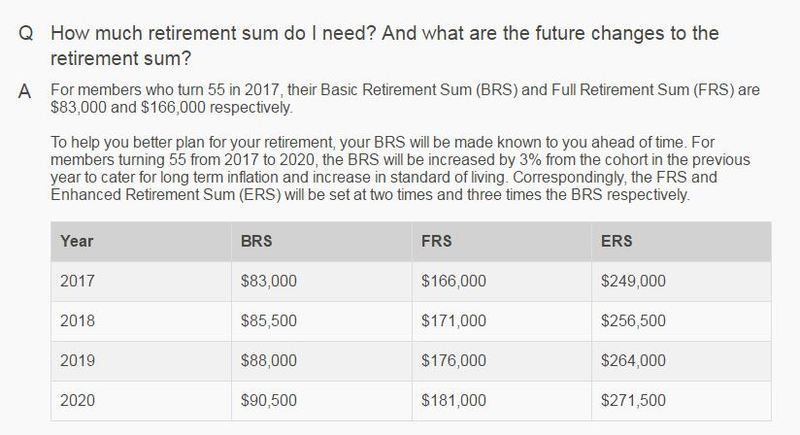

色鹿,別完了BRS,FRS,ERS每年會往上調!

也許你55歲,BRS已經高過100K!

|

|

|

|

|

|

|

|

|

|

|

|

发表于 29-3-2017 06:01 PM

|

显示全部楼层

应该是9万多。

多少都无所谓,如果那递增计划不吸引我的话, 我们选的将会是另外两个。

|

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 4-4-2017 11:01 AM

|

显示全部楼层

色鹿有去聽這個CPF嗎?

色鹿認為下面報導有什麼錯誤?

http://www.straitstimes.com/singapore/treat-cpf-as-fixed-deposit-or-atm

Treat CPF as fixed deposit or ATM?

The Sunday Times Invest editor Lorna Tan shared a tip with a 250-strong crowd who turned up at the askST@NLB talk, held last Friday at Library@Orchard.

Drawing laughter from the audience, she declared: "Before age 55, my game plan is to treat my CPF (Central Provident Fund) like a fixed deposit.

"After 55, it will become an ATM (automated teller machine)."

Titled "What You Need To Know About CPF", her talk was the 11th in the year-long series sponsored by National Library Board (NLB), where readers can learn more about topics ranging from finance to education from ST correspondents.

All the seats were snapped up two weeks earlier.

At the talk, the crowd listened attentively as Ms Tan delved into topics such as CPF interest rates, the Retirement Sum Topping-Up Scheme, CPF withdrawals and CPF Life.

A further 1,500 people watched the live streaming of her talk.

Ms Tan described a quirky habit.

When reading the newspapers' obituary pages, her eyes are drawn to the dead people's ages. Are they younger or older than 65?

The reason for her interest? From age 65, eligible CPF members can start receiving monthly payouts under the CPF Life annuity scheme.

Electrical engineer Low Hong Guanhas previously attended three askST@NLB talks and reads Ms Tan's weekly column in The Sunday Times regularly.

The 43-year-old said: "The talk was very insightful, with a lot of useful information that some of us might be unaware of."

After the talk, he asked Ms Tan if he could transfer the equivalent lump sum in cash that he had used to buy his property into his CPF account to earn more interest.

He found out he could not do so as he had not withdrawn from his CPF savings to purchase his property.

Madam Jo C., 70, a retired teacher, found the part on CPF nominations particularly enlightening.

She said: "Lorna mentioned that CPF savings cannot be distributed by a will, and that the Public Trustee's Office will charge for administering un-nominated CPF money.

"I didn't know that previously, that's why this talk is important."

She added that the talk was informative, and Ms Tan was a clear speaker. The next askST@NLB talk will be given by ST assistant sports editor Rohit Brijnath on April 28.

His topic is "An Athlete's Life: It's A Crazy One".

|

|

|

|

|

|

|

|

|

|

|

|

发表于 7-4-2017 01:52 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

| |

本周最热论坛帖子 本周最热论坛帖子

|

1818

1818  55

55